-

Employer Branding For Niche Industries: Standing Out In Specialized Markets

Niche industries refer to specialized sectors of the economy that cater to a unique target market or deliver highly specific products or services. These industries often require specialized skills and expertise, and examples include biotechnology, aerospace, luxury goods, and many more. In such industries, finding and attracting top talent is crucial for success, as the demand for specialized professionals is high. Therefore, employer branding plays a critical role in niche industries. Creating a strong employer brand helps these companies stand out from their competitors and attract the best talent. However, creating a compelling employer brand within these specialized markets presents unique challenges and opportunities. This article will explore the reasons…

-

5 Reasons Why Creatine Monohydrate Is The Best

Are you looking for a supplement that can help you increase muscle mass, strength, and overall athletic performance? Look no further than creatine monohydrate. With so many options on the market, it can be overwhelming to choose the right supplement for you. However, creatine monohydrate has been widely studied and proven to be one of the most effective and safe supplements available. Creatine monohydrate is a naturally occurring compound that plays a crucial role in the production of energy during high-intensity exercise. It has been used by athletes and bodybuilders for decades to improve their performance and achieve their fitness goals. Reason 1: Increased Muscle Strength and Power Creatine Monohydrate…

-

The Cost Of Hair Transplants: What To Expect

Hair loss is a common concern for many individuals, and with the increasing popularity of hair transplants, more people are seeking solutions to restore their hair. Turkey, in particular, has become a popular destination for hair transplant procedures due to its high-quality services and affordable prices. In this paper, we will explore the cost factors associated with hair transplants in Turkey, aiming to provide a comprehensive understanding of the expenses involved in this procedure. Understanding the cost factors is crucial for individuals considering hair transplants, as it allows them to make informed decisions and plan their budgets accordingly. By examining key factors such as the cost of the procedure itself,…

-

Peso888 Login: Access Exclusive Filipino Gaming Experiences

Peso888 is a premier online gaming platform that offers exclusive Filipino gaming experiences to its users. With a wide range of exciting games and interactive features, Peso888 provides a unique and immersive gaming experience that celebrates the rich art, culture, and traditions of the Philippines. From traditional Filipino games to modern virtual environments, Peso888 offers a diverse array of gaming options that cater to the interests and preferences of Filipino gamers. With a user-friendly interface and seamless navigation, players can easily access and enjoy a variety of games while connecting with other Filipino gamers from around the world. Peso888 is dedicated to providing a safe and secure gaming environment, ensuring…

-

베터의 가장자리: 상위 토토 사이트 식별

온라인 스포츠 베팅에 관한 추측 게임을 하는 데 지치셨나요? 토토 사이트의 세계에 숨겨진 보석을 밝혀내 큰 승리 가능성을 높이고 싶으신가요? 더 이상 보지 마! 이 블로그 게시물에서는 베터로서 최고의 우위를 점할 최고의 토토 사이트를 식별하는 비밀을 깊이 탐구할 것입니다. 게임을 시작할 준비를 하고 전문가 팁과 트릭으로 승리를 극대화하세요. 운이 당신의 운명을 좌우하지 않도록 하세요. 베팅을 통제하고 오늘부터 더 현명한 선택을 시작하세요! 토토베팅 소개 베팅 업계를 강타한 통쾌하고 빠른 스포츠 도박, 토토 베팅의 세계에 오신 것을 환영합니다. 숙련된 베팅가이든 게임을 처음 접하는 사람이든 토토는 흥분과 잠재적인 승리를 위한 무한한 기회를 제공합니다. 토토 베팅은 평균적인 스포츠 베팅 경험이 아닙니다. 전통적인 복권 게임의 요소와 다양한 스포츠 이벤트에 베팅하는 스릴을 결합합니다. 이 독특한 블렌드는…

-

안전한 베팅 방법: 사기 사이트를 피하는 방법

모든 순간에 흥분과 스릴이 기다리고 있는 온라인 베팅의 세계에 오신 것을 환영합니다. 여러분이 노련한 도박꾼이든 그저 이 신나는 영역에 발을 담그는 것이든 간에, 한 가지 확실한 것은 안전이 항상 최우선이라는 것입니다. 의심할 여지가 없는 베터들을 공격할 준비가 된 수많은 사기 사이트들이 그늘에 숨어 있는 상황에서, 지식을 무장하고 이러한 사기 플랫폼을 피하는 것이 중요합니다. 이 블로그 게시물에서는 힘들게 번 돈을 보호할 뿐만 아니라 진정한 기회와 페어 플레이로 가득 찬 잊지 못할 경험을 보장하는 안전한 베팅 관행의 비밀을 알아보겠습니다. 그러니 안전벨트를 매고 온라인 도박의 위험한 물을 헤쳐나갈 준비를 하세요! 온라인 베팅 소개 및 사기 사이트 증가 온라인 베팅 소개 및 사기 사이트 증가 모든 것이 클릭 한 번으로 끝나는 오늘날의 디지털 시대에…

-

Shedding Light On The Dark Side Of Labor: Uncovering Wage Irregularities In Schwarzarbeit

Schwarzarbeit, or illegal employment, refers to work that is not reported to the tax authorities or does not comply with labor or social security laws in Germany. It includes activities such as undeclared work, employment without a work permit, and payment under the table. Schwarzarbeit is a significant issue in Germany, leading to tax evasion, unfair competition for businesses following legal regulations, and exploitation of workers. Uncovering wage irregularities in Schwarzarbeit is crucial for several reasons. Firstly, it ensures fair competition among businesses and protects the rights of law-abiding employers and employees. It also helps to combat tax evasion and the loss of social security contributions, which in turn supports…

-

Q25 Casino: The Right And Perfect Casino For You

Q25 Casino is a renowned and highly esteemed casino recognized for its top-tier gaming experience and state-of-the-art facilities. With a wide range of exciting games and a luxurious atmosphere, Q25 Casino offers an unparalleled entertainment experience for visitors and patrons alike. Whether you’re a seasoned gambler or a casual player looking for a night of fun, Q25 Casino has something for everyone. From the moment you step through its doors, you’ll be greeted with a world-class gaming environment, exceptional customer service, and an array of amenities to ensure your visit is nothing short of extraordinary. Discover what sets Q25 Casino apart as we delve into its offerings, services, and overall…

-

PG Slots: Slots, Direct Website, Not Through An Agent, No Minimum

PG Slots is a popular online slot gaming platform known for its unique features and exciting gameplay. With a wide variety of themed slot games, stunning graphics, and rewarding bonuses, PG Slots has quickly gained a loyal following among online casino enthusiasts. What sets PG Slots apart is its user-friendly interface, seamless gameplay, and high payout percentages, making it a top choice for players looking for a thrilling and rewarding gaming experience. When it comes to playing slots, choosing a direct website is crucial for a secure and hassle-free gaming experience. By opting for a สล็อต เว็บตรงไม่ผ่านเอเย่นต์ไม่มีขั้นต่ำ (direct website, no agents, no minimum), players can avoid the risks associated with…

-

아고다 할인코드로 숙박 시설 업그레이드하기

여행을 계획할 때, 우리는 항상 최고의 경험과 편안함을 추구합니다. 그리고 이제 우리 모두가 알게 된 아고다(Agoda) 할인코드를 통해 이런 업그레이드된 숙박 시설에 머무를 수 있습니다! 여러분은 어떻게 하시겠습니까? 지금부터 당신이 원하는 천국같은 호텔로 이동하기 위한 비법을 소개하겠습니다. 준비되셨나요? 그러면 시작해볼까요! 아고다 및 할인코드 소개 지속적으로 큰 거래를 주시하는 여행 애호가입니까? 더 이상 보지 마세요, 아고다에 대한 흥미로운 소개와 놀라운 할인 코드가 있기 때문입니다! 편안한 해변 휴가나 모험적인 도시 탐험을 계획하시든 아고다가 여러분을 보호해 드립니다. 아고다는 전 세계적으로 수백만 개의 숙박 옵션을 제공하는 원스톱 플랫폼입니다. 고급 호텔부터 아늑한 아파트, 저렴한 호스텔까지 모든 유형의 여행자를 위한 것이 있습니다. 제일 좋은 부분? 아고다의 할인 코드를 사용하면 은행을 망치지 않고 숙박을 잊을 수 없는…

You May Also Like

잠실 최고의 나홀로 명소 탐방 : 잠실 오피스텔의 하이라이트

-

Online Roulette Strategies: How To Increase Your Odds Of Winning At U9Play Casino

Strategies are essential for increasing the odds of winning at U9Play Online Casino, especially for players at the U9 level. The use of effective strategies can greatly improve the chances of success and profitability, as opposed to relying solely on luck. By implementing well-thought-out tactics, such as setting budget limits, learning the rules of the games, and taking advantage of bonuses and promotions, players can significantly enhance their overall gaming experience and potentially secure more wins. Moreover, employing strategies can also help players stay disciplined and focused while playing at U9Play Online Casino. It allows them to make rational decisions and avoid impulsive behavior that could lead to unnecessary losses.…

-

SEO와 소셜 미디어의 상호작용

안녕하세요! 오늘은 모두가 알고 있는 SEO와 소셜 미디어의 힘에 대해 이야기해보려고 합니다. 인터넷 세상에서 높은 검색 엔진 순위를 차지하고, 동시에 사회적 네트워크에서 홍보 및 광고를 하는 것이 얼마나 중요한지 우리는 잘 알고 있습니다. 그러나 SEO와 소셜 미디어 간 상호작용을 최대한 활용하여 온라인 비즈니스를 성공으로 이끄는 방법에 대해서는 아직 많은 사람들이 모르거나 제대로 사용하지 못하는 경우도 있습니다. 이번 포스트에서는 SEO와 소셜 미디어가 어떻게 상호작용하며, 왜 그것이 당신의 비즈니스에 필수적인 요소인지 알아보겠습니다. 함께 살펴볼까요? 소개: SEO와 소셜 미디어의 중요성 온라인 마케팅의 경우 SEO와 소셜 미디어라는 두 가지 중요한 요소가 비즈니스 성공에 크게 영향을 미칠 수 있습니다. 이 두 가지 강력한 도구는 함께 작동하여 브랜드를 새로운 수준으로 끌어올릴 수 있는 시너지 효과를 창출합니다.…

-

The Pros And Cons Of No Deposit Bonus Casinos: Is It Worth It?

Are you a fan of online casinos? Have you ever come across the enticing offer of a no deposit bonus? While these bonuses can seem like a great deal, it’s essential to weigh the pros and cons before diving in. No deposit bonus casinos have gained popularity among online gamblers in recent years. These casinos offer players the chance to play without having to make an initial deposit, allowing them to try out different games and potentially win real money. However, like any other offer, there are both advantages and drawbacks to consider. Considering whether to take advantage of a no deposit bonus? It’s crucial to have a comprehensive understanding…

-

여우알바에서 찾는 유흥종사자의 일자리 전략

연예계에서 짜릿하고 흥미진진한 직업을 찾고 계십니까? 더 멀리 여우알바(여우왈바)의 세계를 보세요! 신나는 직업을 원하든, 여분의 현금을 원하든, 유흥종사자(연예계 종사자)로 일하는 것은 당신에게 무한한 기회를 제공할 수 있습니다. 이 블로그 게시물에서는 이 분야에서 꿈의 직업을 찾기 위한 전략과 성공 방법에 대해 알아보겠습니다. 여우알바 풍경을 탐색하는 궁극적인 가이드와 함께 완전히 새로운 가능성을 발견할 준비를 하세요! 폭스 알바 산업 소개 폭스 알바 산업 소개 환상이 현실과 만나고, 욕망이 이루어지고, 비밀이 속삭이는 세상에 오신 것을 환영합니다. 폭스 알바 산업은 일상에서 벗어나려는 많은 사람들의 마음과 마음을 사로잡았습니다. 하지만 우리가 말하는 이 신비한 세계는 정확히 무엇일까요? 한국에서 시작된 폭스 알바 산업은 최근 몇 년 동안 상당한 인기를 얻었습니다. 그것은 교제와 여가에 대한 파격적인 접근을 제공하는 성인…

-

How To Recover From A Freewallet Scam: Steps To Take if You’ve Been Scammed

Have you fallen victim to a Freewallet scam? Losing your hard-earned money to a scam can be devastating. But don’t worry, there are steps you can take to recover from this unfortunate situation and protect yourself from further harm. Cryptocurrency scams have become increasingly common in recent years, and Freewallet is no exception. Many people have found themselves deceived and robbed of their funds by these fraudulent schemes. However, it’s important to remember that you are not alone in this predicament, and there are resources available to help you navigate the recovery process. Recovering from a Freewallet scam requires swift action and a thorough understanding of the necessary steps to…

-

The Benefits Of Masturbation: Why Solo Sex Is Good For You

When it comes to discussing the topic of masturbation, there can be a lot of stigma and shame attached to it. However, it’s important to recognize that solo sex can actually have numerous benefits for both physical and mental health. Many people are unaware of the positive effects that masturbation can have on the body and mind. In this article, we will explore the various benefits of masturbation and why it should be embraced as a normal and healthy part of human sexuality. Throughout history, masturbation has been a topic shrouded in secrecy and taboo. However, as society becomes more open and accepting, it is crucial to have open conversations…

-

The Must-Have VPNs For Digital Marketers

In today’s digital age, where online privacy and security are of utmost importance, how can digital marketers ensure that their data and online activities are protected? The answer lies in using a Virtual Private Network (VPN). With the increasing number of VPN providers in the market, it can be overwhelming to choose the right one for your specific needs as a digital marketer. Digital marketers are constantly working with sensitive data, conducting market research, and managing online campaigns. It is crucial for them to safeguard their online presence and protect their valuable information from potential cyber threats. This is where VPNs come in handy, providing a secure and encrypted connection…

-

초보자부터 전문가까지: 온라인 카지노 인사이트

온라인 카지노 게임 레벨업 준비 되셨습니까? 흥미로운 가상 도박의 세계에 발을 담그려는 초보자든, 실력 향상을 목표로 하는 경험 많은 플레이어든, 이 블로그 게시물은 여러분을 위해 맞춤형으로 제작되었습니다. 온라인 카지노의 영역을 깊이 파고들면서 성공의 비결을 풀어낼 준비를 하고, 여러분을 신인에서 노련한 전문가로 변화시킬 귀중한 통찰력을 공유하세요. 행운과 전략이 만나는 이 신나는 여정에 함께하고, 진정한 온라인 도박의 달인이 되기 위한 길을 함께 떠나봅시다! 소개: 온라인 도박이란 무엇인가? 소개: 온라인 도박이란? 오락과 여가 영역에서 도박만큼 급격한 변화를 경험한 산업은 거의 없습니다. 한 때 전통적인 오프라인 시설에 국한되었던 온라인 카지노의 출현은 이 오래된 취미에 대변혁을 가져왔습니다. 그렇다면, 온라인 도박이란 정확히 무엇일까요? 온라인도박은 인터넷기반의 플랫폼을 통하여 카지노 게임에 금전이나 귀중품을 거는 행위를 말합니다. 버튼 클릭…

-

사기꾼들을 능가하다: 스포츠 베팅 사기 검증

당신은 스포츠 베팅 사기의 희생양이 되는 것에 싫증이 났습니까? 사기꾼들을 능가하고 어렵게 번 돈을 보호할 수 있는 완벽한 방법을 갈망하십니까? 운이 좋으시군요! 오늘 블로그 게시물에서는 사기꾼들이 은폐를 시도하게 하는 사기 검증 기술이라는 궁극적인 비밀 무기를 공개합니다. 수상한 웹사이트를 해부하는 것부터 수상한 이메일 제안을 해독하는 것까지, 우리는 스포츠 베팅 세계에서 한 단계 앞서나가는데 필요한 모든 팁과 속임수를 가지고 있습니다. 그러니 안전벨트를 매고 펜과 종이를 잡아라. 왜냐하면 이제는 당신의 내면의 탐정을 풀어주고 당신이 이 속임수 게임에서 또 다른 통계가 되지 않도록 해야 할 때이기 때문입니다. 스포츠 베팅 사기 소개 스포츠 베팅 사기에 대한 소개 스포츠 베팅은 수 세기 동안 인기 있는 취미 생활로 팬들이 좋아하는 스포츠 이벤트의 흥분에 더 가까이 다가갔습니다. 불행하게도,…

-

Tips for å Håndtere og Tilbakebetale Forbrukslån på en Klok Måte

Sliter du med å håndtere og tilbakebetale forbrukslånene dine? Slapp av, du er ikke alene. Mange føler seg overveldet av gjeld og er usikre på hvordan de skal håndtere og tilbakebetale lånene sine på en effektiv måte. Men med riktig kunnskap og de rette strategiene kan du ta kontroll over din økonomiske situasjon og betale tilbake forbrukslånene dine på en fornuftig måte. Forbrukslån har blitt stadig mer populære de siste årene, og gir privatpersoner muligheten til å låne penger til ulike formål, for eksempel til å kjøpe bil, pusse opp boligen eller dra på ferie. Selv om slike lån kan gi økonomisk fleksibilitet, følger det også med et ansvar for…

-

잠실 최고의 나홀로 명소 탐방 : 잠실 오피스텔의 하이라이트

잠실 한복판에 숨겨진 보석을 찾아 도심 속 모험에 나설 준비가 되셨습니까? 혼자 여행하는 사람이든, 꼭 필요한 “나”의 시간을 원하는 사람이든 간에, 우리는 당신을 보장해 드립니다. 잠실의 활기찬 오피스텔 현장에서 최고의 단독 명소를 항해할 수 있는 최고의 가이드를 소개합니다. 사색하기에 딱 좋은 고요한 카페부터 탐험을 기다리고 있는 최신 유행의 부티크까지, 여러분을 매혹시키고 더 갈망하게 할 여행을 준비하세요. 그러니 지도를 들고 잠실 오피스텔의 매혹적인 세계로 뛰어들어 보세요! 소개: 잠실이 나 홀로 여행하기 딱 좋은 동네인 이유 소개: 잠실이 혼자 여행하기 딱 좋은 동네인 이유 활기찬 도시 생활과 평온함이 만나는 잠실이라는 번화한 동네에 오신 것을 환영합니다. 한국의 수도인 서울의 중심부에 위치한 잠실은 솔로 모험가들에게 이상적인 여행지로 만드는 다양한 볼거리와 경험을 제공합니다. 잠실은 현대성과…

You May Also Like

아고다 할인코드로 숙박 시설 업그레이드하기

-

Adult Erotic Blog: Tantric Massages Fuengirola

Tantric massage is an ancient practice that aims to awaken both the body and the mind through sensual touch and soothing techniques. It goes beyond the physical sensations, offering a deeply relaxing and transformative experience. At tantricmassagesfuengirola.com, we specialize in providing exquisite tantric massages in Fuengirola, ensuring that our clients indulge in a journey of self-discovery and ultimate pleasure. Our well-trained therapists skillfully combine elements of traditional massage and tantra philosophy, creating a unique experience that stimulates all the senses. Whether you seek relaxation, healing, or a deeper connection with your inner self, our tantric massages are designed to fulfill your every desire. So come and immerse yourself in the…

-

Freewallet Scam Accusations: Fact Or Fiction?

Freewallet is a cryptocurrency wallet service that provides users with a secure and convenient way to store, manage, and exchange their digital assets. With support for a wide range of crypto coins and tokens, Freewallet offers both mobile and web-based wallets for easy access on various platforms. However, amidst the growing popularity of crypto wallets, Freewallet has faced some scam accusations. These allegations have raised concerns within the crypto community, questioning the security and reliability of the platform. The purpose of this article is to examine the validity of these accusations and shed light on whether they are fact or fiction. By conducting a comprehensive review process, we aim to…

-

Ways To Improve Your Chances Of When Playing Sportsbook At Jitutoto777

Jitutoto777 is an online sportsbook that offers a wide range of gambling entertainment options. It provides a platform for casino enthusiasts and passionate sports fans to enjoy their favorite casino games and place bets on popular sports. With its user-friendly interface and a variety of bonuses, Jitutoto777 stands out among the many online casinos and sportsbooks available in the market. This reputable casino allows players to make informed decisions by providing detailed information about the various games and sports it offers. Whether you prefer traditional brick-and-mortar casinos or modern online gambling platforms, Jitutoto777 ensures an exciting gambling experience with real money winnings. From popular casino games to a range of…

-

온라인 카지노에 대한 전체 가이드: 바카라, 슬롯 등

온라인 카지노의 모든 것을 위한 궁극적인 가이드에 오신 것을 환영합니다! 바카라, 슬롯 또는 다른 카지노 게임의 팬이라면, 이것이 당신을 위한 블로그 게시물입니다. 우리는 평판이 좋은 사이트를 찾는 것에서부터 인기 있는 게임과 전략을 숙달하는 것까지 여러분이 온라인 도박에 대해 알아야 할 모든 것을 정리했습니다. 온라인 카지노의 세계를 처음 접하든, 숙련된 프로든, 우리의 완전한 가이드를 계속 읽고, 그 가상 테이블들을 멋지게 칠 준비를 하세요! 온라인 카지노 소개 온라인 카지노의 세계는 초보자들에게는 벅찬 것이 될 수 있지만, 걱정하지 마세요! 기술과 인터넷의 발달로, 여러분이 가장 좋아하는 카지노 게임을 하는 것이 그 어느 때보다 쉬워졌습니다. 가정의 편안함이나 모바일 기기로 이동 중에 도박과 함께 오는 모든 흥분과 보상을 경험할 수 있습니다. 온라인 카지노는 바카라와 블랙잭과 같은…

-

Wireless Fence For Dogs

A wireless fence for dogs is an alternative to traditional fencing that allows dogs to safely roam and play within set boundaries without physical barriers. It uses a radio signal transmitted from an indoor transmitter to a receiver collar worn by the dog, which emits a warning tone when the dog approaches the boundary. If the dog continues to move closer to the boundary, it receives a static correction to discourage it from crossing. Wireless fences are a convenient and effective solution for pet owners who want to keep their dogs safe and secure within a specific area. Benefits of a Wireless Fence for Dogs Wireless fences for dogs can…

You May Also Like

Best Collars To Train A Dog

-

Best Collars To Train A Dog

When it comes to training your furry friend, selecting the right collar is essential. With the wide range of collars available, it’s essential to choose one that provides effective training while also being comfortable and safe for your dog. In this article, we will provide you with an overview of the best collars available to train your dog. We will discuss the types of collars, their features, and the benefits of using each one to help you make an informed decision that best suits your pet’s needs. Types of Training Collars Training collars are a helpful tool for pet owners looking to reinforce positive behaviors and correct unwanted habits in…

You May Also Like

Wireless Fence For Dogs

-

Play Lottery Gambling With Jitutoto Now

Jitutoto is an online lottery platform that offers a new and convenient way to play your favorite lottery games from anywhere in the world. With millions of players spanning different countries, Jitutoto provides a fun and exciting way to participate in lotteries with a chance to win big. Powered by state-of-the-art technology and a user-friendly interface, Jitutoto has become a popular platform for those looking to try their luck in lotteries and potentially change their lives. Read on to learn how to play lottery gambling with Jitutoto. Overview of Play Lottery Gambling With Jitutoto Now Gambling on Jitutoto is a great way for players to have fun and possibly win…

-

Why You Should Try Gold Ira Investments

A Gold IRA is a retirement account that permits investors to keep physical gold or other precious metals in their portfolio. Unlike traditional IRAs that invest in mutual funds or stocks, Gold IRAs provide investors with the opportunity to have tangible assets that act as an inflation hedge and store value during economic uncertainty. Additionally, Gold IRAs offer tax advantages and can be self-directed, enabling investors to take control of their retirement savings and invest in physical assets through an IRS-approved depository and trust company. Exploring the advantages of investing in a Gold IRA. Investing in a Gold IRA is becoming increasingly popular as retirees look for new ways to…

-

재미있는 온라인 카지노 게임으로 크게 성공하세요

당신을 초조하게 해줄 스릴을 찾고 계십니까? 온라인 카지노 게임보다 더 멀리 보지 마세요! 선택할 수 있는 무한한 옵션이 있는 이 흥미로운 게임들은 실제 카지노의 모든 흥분과 매력을 경험하면서 크게 이길 수 있는 기회를 제공합니다. 여러분이 노련한 도박꾼이든 아니면 단지 높은 판돈을 걸고 재미를 찾고 있든 간에, 여러분이 승자처럼 느끼게 해줄 몇 가지 꼭 해봐야 할 온라인 카지노 게임들이 있습니다. 그러니 여러분의 행운의 매력을 잡고 스릴 넘치는 온라인 즐겨찾기로 대박을 터뜨릴 준비를 하세요! 온라인 카지노 게임 소개 만약 여러분이 크게 이길 수 있는 스릴 있고 흥미로운 방법을 찾고 있다면, 여러분은 반드시 온라인 카지노 게임을 확인해야 합니다! 그것은 빠르고 쉬운 돈을 얻는 좋은 방법이고, 또한 매우 재미있습니다! 선택할 수 있는 다양한 온라인…

-

A Guide To Big Picture Loans

Are you looking for a loan that can help provide financial stability? Big Picture Loans is the ideal solution for those who need an immediate cash infusion. With competitive interest rates, flexible repayment options, and quick approval processes, Big Picture Loans reviews have praised its services and benefits. Read on to learn more about the advantages of choosing Big Picture Loans and how to apply for one. What Is Big Picture Loans? Big Picture Loans is an online lender that offers secured and unsecured loans to individuals with a variety of credit profiles. The company specializes in providing short-term, small-dollar loans with flexible repayment options. It also helps customers who…

-

The Impact Of Flex Group Dallas Real Estate

Are you interested in investing in Dallas real estate, but don’t know where to start? Flex Group Dallas has revolutionized the way people buy and rent properties in the area. From office space to property managers, this innovative company offers a variety of services that have had a major impact on the Dallas real estate market. In this article, we’ll explore how Partners Real Estate and other flex spaces are changing the landscape of Dallas and what it means for residents. So if you’re curious about what’s happening in Dallas’ booming real estate industry, then read on! What is Flex Group Dallas? Flex Group Dallas is a real estate company…

You May Also Like

Veranda Design Ideas

-

Tips For Beginners Who Are Playing At An Online Casino

Are you a beginner looking to try your luck at an online casino? The thought of taking on the unknown may seem daunting, but with these tips for beginners who are playing at an online casino, you can successfully navigate the world of digital gambling. From creating an account and verifying your identity to understanding different types of casino games and bonuses & promotions offered by online casinos, this guide has everything you need to start winning big! With the right mindset, knowledge, and resources, there’s no limit to what you can achieve. So let’s get started! Getting Started Getting started with online gambling is fairly simple, but there are…

-

Tips To Win Sports Betting

Sports betting is an adrenaline-charged way to make money from the comfort of your own home. For some, it’s a form of entertainment; for others, it’s a great way to generate income with relatively low risk. But if you want to win at sports betting, there are certain rules and strategies you must follow. With the right approach, you can maximize your chances of success and start earning big! So, if you’re ready to get started on your journey to becoming a professional sports bettor, read on for our top tips to win sports betting. What is sports betting? Sports betting is a form of wagering on the outcome of…

-

Online Slot In Megaways

Are you ready to take a chance and experience the thrill of online slots? Megaways slots are taking the online gambling world by storm, offering players a unique opportunity to spin and win big. With cascading reels, bonus features, wild symbols, and more, this type of slot game is bound to captivate even the most experienced gambler. In this article, we will cover all you need to know about the exciting world of Megaways slots – from popular games to bonus features and how to play responsibly. So if you’re ready for an adventure that could change your life, read on! Definition of Megaways Slots Megaways slots are new online…

-

How To Win In Poker Non Gamstop Casinos

Are you a poker enthusiast looking for ways to increase your chances of winning at non-Gamstop casinos? If so, then you’ve come to the right place! Poker is one of the most exciting casino games and can be incredibly lucrative if played correctly. With the right strategies and techniques, you can turn your luck around in no time. From learning the basics of the game to understanding how to take advantage of bonuses and promotions, this article will provide you with essential tips on how to win at non-Gamstop casino poker games. So what are you waiting for? Get ready to become an expert poker player! Strategies for Winning at…

-

CBD Legal Status By States

Cannabidiol (CBD) is one of the most popular natural remedies used to treat a variety of ailments, but its legal status varies from state to state. With so much confusion swirling around cannabis-derived products, it’s important to understand the differences between hemp- and cannabis-derived products and the regulation surrounding them. From heavy metal content requirements to labeling requirements for dietary supplements, this article will explore the complex legal landscape of CBD use by the state. Overview of CBD Legal Status by States CBD is a cannabinoid found in the cannabis plant, which can be derived from both hemp and marijuana. Hemp-derived CBD contains very low levels of the psychoactive compound…

-

What Are The PBN Website Example

Building a successful online business takes time and dedication, but there is a shortcut you can take: creating and managing your private blog network, or PBN. By harnessing the power of PBNs, you can quickly increase your website’s visibility in search engine rankings and generate more qualified leads. In this article, we’ll discuss what PBNs are, different types of PBNs, best practices for building and managing a PBN website example, and how to monitor your backlink profiles. With the right resources and strategies in place, you can give your website the boost it needs to be successful. Why PBNs are Used Private blog networks, or PBNs, are used by marketers…

-

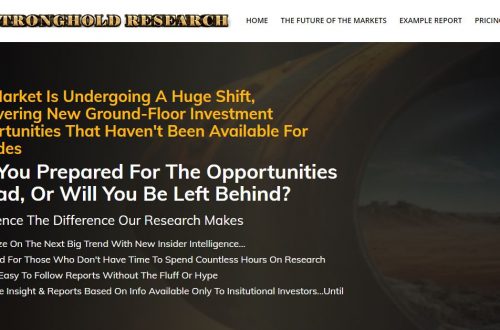

Stock Market Research For the Future

The stock market is constantly shifting, so it’s essential to stay abreast of the newest developments. With accurate information at your disposal from Stronghold Research, you can make informed decisions regarding your investments with confidence. Effective stock research employs a combination of fundamental, technical and sentimental analysis. Comprehending these three techniques will give you a deeper insight into your portfolio and enable you to make more informed investment decisions. Fundamental Analysis Fundamental analysis can be an effective tool for researching stocks for the future, helping you uncover undervalued securities that could prove profitable investments in the long run. Undervalued stocks often end up being wise investments that will “catch up”…

-

9 Life-saving Tips About Online Betting Sites

The online world of sports betting can be a confusing and dangerous place for the uninitiated. There are so many different sites and options available that it can be tough to know where to start, or even where to bet. That’s why we’ve put together this list of 9 life-saving tips for betting on sports online. By following these tips, you’ll be able to stay safe while still enjoying the thrill and excitement of betting on your favorite sports. 1. Do your research This is the most important tip on the list. Before you even think about placing a bet, you need to do your research and make sure that…

-

Risks and Rewards of Refinancing Your Loans

Refinancing your loans can save you money on interest costs and enable you to pay off debt faster, but there are risks you should weigh before making the move. Refinancing your home allows you to access a substantial portion of its value without selling, which could be beneficial if you need extra funds for education expenses, home improvements, or starting a business venture. 1. Interest Rates Refinancing your loans requires an assessment of your financial situation in order to secure more favorable borrowing terms. Consumers often refinance their mortgages, car loans, and student loans in response to shifting economic conditions. Interest rates are an integral component of the refinancing process.…

-

7 Proven Facts That Viagra Can Help

Viagra is a medication that’s used to treat erectile dysfunction (ED), a condition where you don’t have an erection when you want it. It works by interacting with chemicals in your body that helps your penis become hard and erect. Some people also take Viagra to reduce feelings of anxiety, depression, or nervousness that can cause ED. Talk to your doctor if these feelings interfere with your ability to have an erection. 1. It Helps You Get an Erection There are a number of reasons why men may have trouble getting an erection, and many of them can be treated with medications like Viagra. These drugs work by blocking a…

-

Do You Need Viagra to Treat Erectile Dysfunction?

Whether you’re struggling with erectile dysfunction (ED) or not, it’s important to talk to your doctor about whether Viagra is right for you. While it can help, Viagra doesn’t cure ED. It’s also not a good choice for people with serious medical conditions, such as heart disease or high blood pressure. What is erectile dysfunction (ED)? ED is one of the most common problems men have with sex. It occurs in about 1 in 5 men and is more likely to occur with age. Normally, when a man gets sexually aroused, nerves, muscles, and hormones work together to create an erection. When a man experiences ED, the nerves, muscles, and…

-

Planting Vine Plants in Your Garden

Vines are a wonderful addition to any garden. They provide beauty and interest, and can even be used to create privacy or shade. Vines can be trained to grow on fences, trellises, arbors, or even left to grow freely on the ground. There are many different types of vines to choose from, so you’re sure to find one that will suit your needs. When planting vines, make sure to choose a location that gets plenty of sun and has well-drained soil. Vines need room to spread out, so give them plenty of space. It’s also a good idea to add a trellis or other support structure when planting. This will…

-

Veranda Design Ideas

If you’re looking for veranda design ideas, you’ve come to the right place. A veranda is a great addition to any home, and can provide a wonderful space for entertaining, relaxing, or simply enjoying the outdoors. There are a variety of veranda designs to choose from, and the best way to find the perfect one for your home is to browse through some photos and get inspired. Once you have an idea of what you want, you can start planning your own veranda design. One of the most important things to consider when designing a veranda is the layout. You’ll need to decide how much space you want, and where…

You May Also Like

The Impact Of Flex Group Dallas Real Estate

-

Benefits of Vitamin D in Our Body

Vitamin D is an important nutrient that our body needs in order to stay healthy. It helps our bodies absorb calcium, which is essential for strong bones and teeth. Vitamin D also helps protect us from diseases such as osteoporosis, heart disease, cancer, and diabetes. There are many ways to get vitamin D. Our bodies make vitamin D when our skin is exposed to sunlight. We can also get vitamin D from certain foods such as fatty fish, eggs, and fortified milk and cereals. Some people may need to take a supplement to get enough vitamin D. The health benefits of vitamin D are well-established. Vitamin D helps our bodies…

-

Pros and Cons of Using Astringents

Astringents are solutions that cause the contraction of body tissues. They are either applied topically or used as a gargle. Astringents work by constricting body tissues, which leads to a decrease in secretions and inflammation. There are several pros and cons to using astringents. Some of the pros include: -Astringents can help to cleanse the skin and remove dirt, oil, and makeup. -They can help to shrink pores and reduce the appearance of blemishes. -Astringents can help to control excess oil production. -They can help to tone and tighten the skin. Some of the cons of using astringents include: -Astringents can cause dryness, redness, and irritation, especially for those with…

-

Popular Online Casino Games for Beginners

There are many different types of casino games that you can play online, but some are more popular than others. If you’re new to online gambling, it can be a bit overwhelming trying to figure out which games to play. But don’t worry – we’re here to help! In this blog post, we’ll give you a rundown of some of the most popular online casino games for beginners. One of the most popular casino games is slots. Slots are easy to play and there’s no need to learn any complicated rules. Just spin the reels and hope for the best! There are many different themes and variations of slots games,…

-

Best Mobile Shooting Game

Mobile shooting games are some of the most popular and lucrative games on the market. They’re perfect for when you need a quick fix of gaming, and they’re usually packed with lots of action and excitement. There are loads of different mobile shooting games to choose from, so we’ve put together a list of some of the best ones that you can play right now. 1. Call of Duty: Mobile Call of Duty: Mobile is one of the most popular mobile shooting games around, and for good reason. It’s packed with fast-paced action, intense gunfights, and plenty of things to do. The game features a variety of different modes, including…

-

Giving Gifts for the Elders

Giving gifts to the elders is a great way to show your respect and appreciation for their wisdom and experience. It can be difficult to find the perfect gift for an elder, but there are some general guidelines that can help you choose a thoughtful and meaningful present. Think about the things that the elder in your life enjoys. What are their hobbies or interests? Do they prefer practical items or something more sentimental? Consider what would make them happy and feel appreciated. It’s also important to think about the elder’s current situation. Are they living independently, in assisted living, or in a nursing home? If they’re not able to…

-

Cheapest Gifts for your Friends

When it comes to finding the perfect gifts for your friends, it’s important to think about what they would really appreciate. After all, your friends are some of the most important people in your life, so you want to make sure they know it! However, you may not have a lot of money to spend on gifts, which is why we’ve compiled a list of the cheapest gifts that your friends will still love. 1. A handwritten letter. Sometimes, the most thoughtful gift is something that you took the time to write yourself. A handwritten letter is a great way to let your friend know how much they mean to…

-

Different Ways to Invest Your Money

There are many different ways that you can invest your money. You can put it into a savings account, which will grow over time as you add more money to it. You can also invest in stocks, bonds, and other securities. These can provide you with income, but they also come with risks. You can also invest in real estate. This can be a good way to earn income, but it also comes with its own set of risks. You need to be aware of the market and of the properties that you are interested in before you invest. You can also put your money into a business. This can…

-

Things to Consider Before Investing

When it comes to investing, there are a lot of things to consider before taking the plunge. Here are just a few things to keep in mind before investing your hard-earned money: 1. Your goals – What are you looking to achieve through investing? Are you trying to grow your wealth, generate income, or both? Your investment goals will help guide your decision-making process and ensure that you’re investing in the right types of assets. 2. Your risk tolerance – How much risk are you willing to take on? This is an important question to ask yourself, as it will dictate the types of investments that are suitable for you.…

-

A Beginner’s Guide To Stocks and Shares

he stock market is a network of trading exchanges where investors buy and sell shares in publicly traded companies. Whether you’re a long-term investor or a short-term trader, understanding how the stock market works is essential to building your portfolio and making money from it. Types of Stocks and Shares In the world of investing, there are a few different kinds of stocks to choose from, including common stocks and preferred stock. Each type has a different set of characteristics and benefits that can help you make the right investment decision. Common stocks grant shareholders voting rights, a chance to participate in company earnings, and the ability to earn dividend…

-

Personalized Charcuterie Board: A Perfect Gift For Her

When it comes to finding the perfect gift for her, look no further than a personalized charcuterie board. Whether you’re looking for a unique way to show your appreciation on Valentine’s Day or you want to give something special for a birthday, Mother’s Day, or anniversary, this delightful gift is sure to make her smile. From standard shipping boards and bamboo cheese boards to custom cutting boards and engraved cutting boards, there are so many options for creating the perfect personalized charcuterie board. Let’s take a closer look at why these delightful gifts are sure to impress – and how you can create one that will make her swoon! Why…

IRAN INVESTMENT

برای سرمایه گذاری مطمئن